Tasco expected to make plans to capitalise on recovery

Tasco Bhd

(Jan 20, RM1.20)

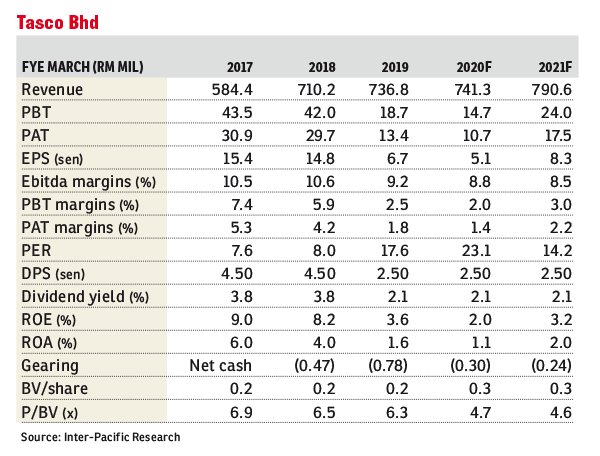

Maintain hold with a target price (TP) of RM1.17:Our “hold” call for Tasco Bhd is maintained with a TP of RM1.17, pegged at a price-earnings ratio of 14 times to our financial year ending March 31, 2021 (FY21) earnings per share forecast of 8.3 sen, from 9.2 sen previously, as we account for a lower sales growth in Tasco’s cold supply chain segment and delays in the Hai San acquisition, coupled with the management’s outlook guidance.

Tasco views the industry is currently in a transition period, a chance to rebuild resources, ahead of the economy picking up over the medium term. A case in point: Neighbouring industry players such as Hap Seng Consolidated Bhd and Mapletree Logistics Trust, also located in Shah Alam, are continuing to expand their warehousing capacities despite the economic slowdown.

The management has plans to expand and improve Tasco’s warehousing capabilities to reduce manual labour. This may include a conveyor system and/or an automated storage and retrieval system. The expansion is approximated to cost RM200 million to RM250 million. The construction is planned to commence in mid-2020, with an estimated completion of two years. Financing details are still being ironed out.

Narrower losses are expected for the retail convenience logistics for FY20 and it looks to break even in FY21. This will be from better operational efficiency, reduced manpower and rent costs from using third-party premises for its operations. Tasco looks to further scale into this segment by bringing in new customers. Issues arising from Hai San’s liquidation have delayed the Port Klang cold warehouse acquisition. However, the acquisition is to proceed and expected to be completed within six months. Earnings contribution from the new capacity will only appear in FY21.

The company noted the current year’s performance remains largely tepid or could be slightly better than in the previous year as some geopolitical uncertainties are closer to being resolved. — Inter-Pacific Research, Jan 17

( 24,36 % )

( 39,38 % )

( 36,26 % )